With a little spoiler, the answer is: fortunately, not much!

While having a competitive price is important, the main drivers of online conversion are elsewhere. The context in which we humans make a choice is a powerful driver of our decisions, and this is true for online insurance as well.

The article below focuses on the content of the webpages hosting online portals and their key messages framing. The boost in conversion rate generated by the right context is staggering, and it outperforms price slashing by quite a margin. Let me explain why.

“Most people don’t know what they want unless they see it in context.” Dan Ariely

What do BigFoot and Homo Economicus have in common?

In the last few years, the insurance industry has come to the realisation that getting their products online is an absolute must. Especially in the post-Covid world, where the pandemic reinforced “the urgency of accelerating product innovation and digital transformation” (McKinsey, 2020).

However, one of the consequences of the products’ digitalisation is that the insurers seem to face harder competition on price. Aggregators offer an easy way to instantly compare the price of many insurance products. Even in markets where aggregators are not the standard, consumers can still look around on several websites and obtain quotes from several insurers in a few minutes.

One of the main answers of the insurers to this pressure has been increasing attention (and spending) on risk and price modelling. It is one of the most traditional assumptions of Economics: The better the price offered, the more the consumers will buy, right?

When we encounter such automatic reactions from an entire industry based on the standard economic theory — which has its roots in the 1700s and has been proven flawed time and time again throughout the last couple of centuries — we in Penni.io see it as our job to investigate what is the truth. Also, the insights might give our clients the edge needed to win the fierce online market competition.

The fundamental problem with the standard economic theory is the answer to this section title. What do BigFoot and Homo Economicus have in common? That both of them are tenacious myths even though nobody has ever seen either of them.

We tested if the industry’s convenient assumptions hold any evidence in today’s digital world, or whether it is just a matter of the inside-out perspective and the underwriting industry reverting to the known tools. We gathered and analysed 25 million data points coming from the partners on our Penni Connect SaaS platform. Let’s see what story the data are telling us.

Price matters, but not as much as you would think

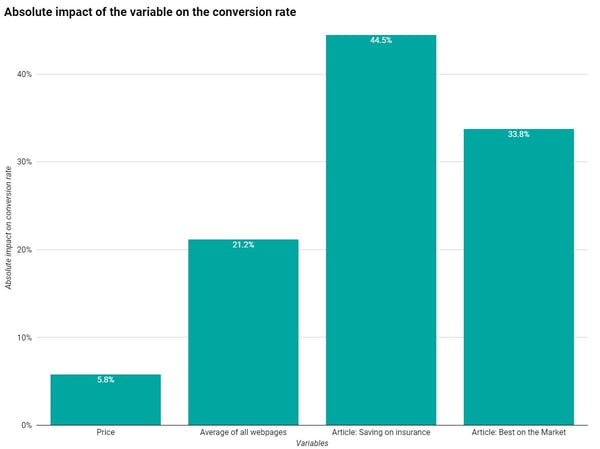

So what I did was look at all the different variables in a customer journey: product-related variables such as excess amount, marketing-related variables such as campaigns and direct emails, environment-related variables such as devices and webpages, and customer demographics such as age. Then I estimated the impact of those variables on our target “Conversion” with several multivariate regressions. To give an example, I chose the results for a motor insurance solution.

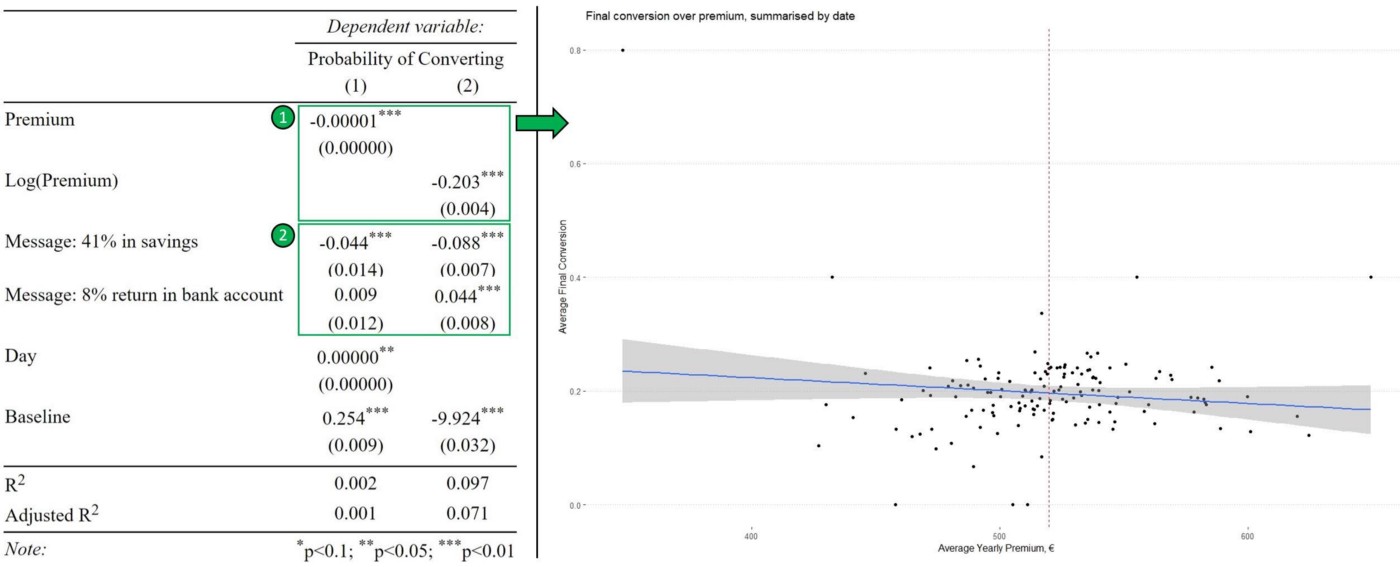

What you can see here are two regressions (the columns) that estimate the correlation between the price in €/year, also referred to as premium, and the conversion rate as the probability of the customer purchasing the insurance once they see the price.

The first is a linear probability model, the second is a level-log probability model. The rows represent the variables and the main numbers are the coefficients for those regressions. These coefficients estimate the impact that the variables have on the conversion rate. The stars next to these coefficients represent the significance level. For explanatory purposes, significance levels can be seen as the probability of the variable having a meaningful, or relevant, impact on the conversion rate (* = 90% probability of being relevant, ** = 95% probability, *** = 99% probability). If there is no star then the variable is likely to not have a truly meaningful impact.

As you can see in box #1 from the three stars next to premium coefficients, the price is significant at 99% level, meaning that both the regressions recognise the premium as having a relevant impact in converting the customers. But how much is this impact? When we multiply the coefficient of the first regression with the average purchasing price for our partners — 528 €/year — the decrease of the conversion is 5.81%. This relationship is negative in the regression because a higher price corresponds to a lower demand.

To put this in perspective, if our client would give a discount of, for example, 100 € to all their potential customers, it would increase the conversion rate by only 5.1%. It would result in the conversion rate rising from 6.3% to 6.6%. Translated, the price has a relevant impact on the sales as we would expect from the classic “the lower the price, the higher the demand”, but its incidence appears somehow limited.

An interesting insight from box #2 is that when you communicate discounts and savings in percentage to your customers you do not significantly boost your sales conversion… when you are lucky and it does not decrease! Telling the customers they would save 41% by switching to their insurance decreased our partner’s conversion from the base 6.3% to 6.0%. I will examine why and how this happens in my next article. For now, consider that percentage discounts on the price are not of big help toward conversion.

Why we buy!

Remember back in the 70s when everybody thought the brain was a computer?

We have just seen that price does matter in terms of converting the customers online, but not so much. But how is it possible? The answer: The brain is not a computer and does not process unlimited information. As Randy Gallistel — an esteemed professor in behavioural and cognitive neuroscience — frames it:

If the brain computed the way people think it computes, it would boil in a minute.

Insurance is a complex and abstract product with which customers rarely interact. And there is little to no reference point out in the real world we can base our insurance purchasing decisions on.

So what do we do when we are lost in the void, with only hard mathematics on price and risk as a reliable guide? We humans really like to skip all the steps involved in solving the equation above and save mental energy, basing our choices on mental shortcuts and seemingly irrelevant contextual elements. And the more complex is the decision, the more we are inclined to do so (Thaler & Sustained provide numerous examples of this phenomenon in their classical book Nudge: Improving Decisions About Health, Wealth, and Happiness).

The avoidance of this complexity makes us shift our decision strategy from aiming for the right decision to aiming for what feels like a good enough decision. And the price has little connections to this feeling.

If you are looking for a deeper walkthrough on humans’ decision-making while buying insurance, I suggest the series of articles “Insurtech: A Sneak Peek at How Customers Decide to Buy” from my colleague Simon Bentholm (here the first volume).

How do customers decide to buy an insurance product online?

So where to focus your efforts? What matters more than price?

Now is finally the time to look at a more effective element than price to make us buy insurance: The context. More specifically, the framing of the message delivered through the website where the insurance offer is placed.

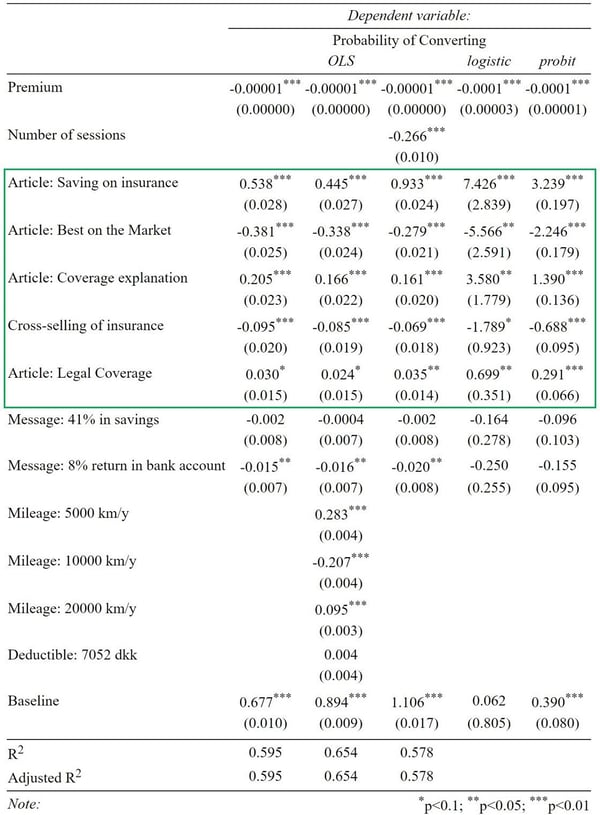

An example from one of our partners helps to make this analysis concrete. The partner has widgets for the purchase of their motor insurance on six different web pages.

The first is the classic main page, with a wide insurance widget that drives focus on the opportunity of purchasing insurance. Four of the other web pages contain articles with different messages, all to help the customers make an informed decision. The last one cross-sells motor insurance with another lower-priced insurance product. The variables related to these web pages are in the green box in the regressions below.

Aside from the article on legal coverage, all the other web pages are highly significant at 99% level. Once again, the regressions individuate the web pages as a relevant factor in driving conversion. But it’s the magnitude of their impact which is incredible. We will take the second regression, the most complete and reliable, as the basis to explain the analysis.

The first webpage “Article: Saving on insurance” increases the probability of converting a customer by 44.5%. Yes, 44.5%. It boosts the base conversion rate of 6.3% on the main widget to 9.1%. This result appears even more amazing if you consider what the article figured on the webpage is about. It does not try to sell you the motor insurance of our partner. It does the opposite, at least apparently.

This first article contains several pieces of advice on how to save on insurance and all of them involve contacting and obtaining a quote from several insurers. After the comparison, it even advises calling your current insurer and asking if they can match the best offer from the other insurance companies. It never mentions buying from our partner. And yet the conversion rate rockets by 44.5%.

Before explaining what this webpage got right, let us see what happens when the webpage gets it wrong.

The second webpage “Article: Best on the Market” has a negative impact on the conversion of 33.8%. It brings the conversion rate to 4.2% from the original baseline of 6.3%. The article tells you how our partner just won a prize for having the best and cheapest insurance proposition on the market.

The reasoning is short and direct. It explains the reasons for the prize and then goes directly to the point: Buy from us because we are better and cheaper than anyone else. The result is that customers read it and then buy less than they would have done normally on the main widget.

Without going too much into detail about the theory behind it, our hypothesis at Penni.io is that this is (mainly) a consequence of the framing effect. With this term, behavioural science refers to “influence on the decision-making of the descriptions of acts, contingencies, and outcomes” (Malenka et al., 1993).

Without going too much into detail about the theory behind it, our hypothesis at Penni.io is that this is (mainly) a consequence of the framing effect. With this term, behavioural science refers to “influence on the decision-making of the descriptions of acts, contingencies, and outcomes” (Malenka et al., 1993).

In our partner’s case, the same choice — to buy the insurance policy — is presented with the same underlying message: We are cheaper than the others, you can trust us. However, they are presented with completely different framing.

In the first case, the partner is giving all the tools and information necessary for the customer to verify the validity of the message. They do not even directly advise to buy their product. The implicit message is: This is not needed because the customers will realise it by themselves once they start comparing prices.

By doing this, our partner is also apparently putting implicit trust in the customers, in their capacity to act on and process the information available. And the customers feel informed and savvy as a result. Then they will likely fail to act upon it because humans tend to save time and mental energy if it is not strictly necessary to do otherwise. But the customers are not self-aware of the tendency, and the positive feeling of being informed stays.

In the case of the second article, the framing is the opposite. They are asking the customers to blindly trust them over a prize won from an organization that is likely unknown or at least vague in the mind of the people reading. And then the partner suggests directly to buy, without any further proof. And customers do not like it.

Context is powerful and is cheap to exploit

Think if the same result of the article with saving suggestions was to be achieved by decreasing the price. To boost the conversion rate from 6.3% to 9.1% it would take approximately a flat discount of almost 380 € on every customer. Without having to make the calculation, directing more customers to the right webpage is definitely a much cheaper option and has the side effect of increasing the trust toward your organisation.

So yes, to sell insurances online the price matters. But not that much: The context matters more.

“Just as no building lacks an architecture, so no choice lacks a context.” Thaler & Sustain, 2008

Free Download: Embedded Insurance Index - Part I

Special thanks to our expert Francesco Cocozza.