Being in a highly competitive market, insurance companies depend on their customers' satisfaction and loyalty. However, many insurers hunt for the bad apples without being aware that they scare off the ‘good’ customers and evidently kill conversions.

If you work with online insurance, you’ve probably heard this riddle:

What’s the difference between an underwriting journey and a customer journey?

Sales.

Most people know the value of having a nice, easy, and intuitive digital customer journey. However, knowing this isn’t the same thing as actually implementing it. That’s why so many digital insurance solutions are still built around inadequate customer journeys.

Customer journey versus underwriting journey

Let’s start with a couple of definitions to make sure we’re on the same page.

A customer journey is the journey users go on when they calculate, choose, and obtain insurance products. In the industry, it goes quote-to-bind, and in the digital world, it’s calculate, modify, and checkout. The customer journey is centred around making it as easy as possible for the customers to get insurance. If you’re good enough at this, you might even destroy traditional market mechanisms.

An underwriting journey is the path insurers, distributors, and brokers go on when gathering data on the customer to calculate the risk of insuring that customer. The underwriting journey is focused on getting the right information and nailing down the exact level of risk. If you excel in this, you can destroy the traditional market mechanisms that were dominant before insurance went digital.

Now, no customer is going to have any interest in handing over a perfect dataset to the insurer. What they want is coverage to protect an object, a process, or a person they value.

A successful online insurance solution, then, will have to start with an intuitive customer journey that offers ease and convenience. The underwriting journey is important, of course, but it will have to be moulded to that customer journey.

I’ve created hundreds of online insurance customer journeys and have never heard anyone object to that. Despite that unanimous approval, however, there are 2 crucial pitfalls that online insurance providers often stumble into. Let’s take a look at them.

Pitfall #1: The legacy

It should be simple: Insurers need to make the customer journey more accessible. So, why not just hire experts from outside the industry to improve their digital solutions?

In theory, that should work like a dream. The reality, however, is not so simple. Working with customer journey experts often means running into a common and hard-to-overcome problem: Legacy systems and products.

A legacy system is like a tripwire running through the core parts of an organisation, ready to mess up your attempts to update and digitise your processes. Unfortunately, it can’t be removed simply by hiring people to handle the digital side of things.

First, when dealing with an old product, the risk is based on a given dataset for each potential customer. Changing the variables in that dataset would be like throwing out valuable intellectual property.

Next is the fact that these datasets are structured in the insurer’s core systems, which can make it impossible to price a product and give a quote without knowing the potential customer’s name.

Finally, the company’s product experts are hired to calculate risk - not to make those risk calculations customer-friendly. Even if you’re making new products that are completely legacy-free, the people making those products won’t be focused on what goes on in the sales channels.

Pitfall #2: Inside-out perspective (or is it the other way around?)

How can you deal with these legacy issues, then?

The answer is not to start all over. There are simpler, more cost-effective, and more effective ways to bridge the customer journey and the underwriting journey.

First, you need to hire product and legal professionals to ensure that a customer dealing with an agent doesn’t have the hassle of answering 25 questions just to get a quote for one of your products. Most potential customers will close the browser if they can’t get a quote after answering three or four questions at most.

Because of that, you need to make sure you’re asking only the essential questions upfront. To do so, you have to divide each interaction in the customer journey into three categories:

- Tarifications: Information that affects pricing.

- Checkouts: The needed information to sign customers into the system.

- Hard stops: Information legally required to approve the sale of the insurance product.

You also have to consider the questions from the customer’s perspective. When facing a question, customers will ask themselves at least three things:

- What’s in it for me? The customers looking for a quick and simple quote will get impatient when they’re asked seemingly irrelevant questions upfront.

- Is it a reasonable question to ask? “How many square meters is your wooden veranda?” might help you give an extremely fine-tuned price, but it won’t seem reasonable to the customer who just wants a quick estimate.

- Can I answer it? Often, customers are asked questions that they can’t answer easily without the help of external tools - e.g., how many kilometres will you drive next year? Or even simpler: What is your odometer reading?

You’re not surprised that these questions pop into your customers’ heads, are you? Of course, the questions you ask your customers should be (easily) answerable, but that’s not always the case. That’s because people in the industry often are blinded by their own interests and beliefs when asking those questions instead of seeing them from the customer’s point of view.

One of my favourite examples is a standard question asked by pricing motor insurances: “How many miles/kilometres are you going to drive next year?”

Most people in the insurance industry won’t bat an eye if you slip that question into the customer journey. But it’s impossible to answer that question since most customers think that not providing an exact answer might mean committing insurance fraud.

And yes, working out all the kinks in your customer journey will have some impact on your time to market. You might have to iterate one or two more times with your Product, IT, and Legal departments. But it’s better to hit the market with a solution that actually converts.

Trying to jump over the pitfalls: Tools at your disposal

To bridge the gap between your customer journey and your underwriting process, you’ll need data. Specifically, you’ll need data on usage in your digital channels and the variety of products being purchased - not only digital ones but also those sold through traditional channels.

Most insurers don’t collect this kind of data in any substantial way. To make up for it, they ask their customers even more questions. However, these additional questions cost the insurers potential sales.

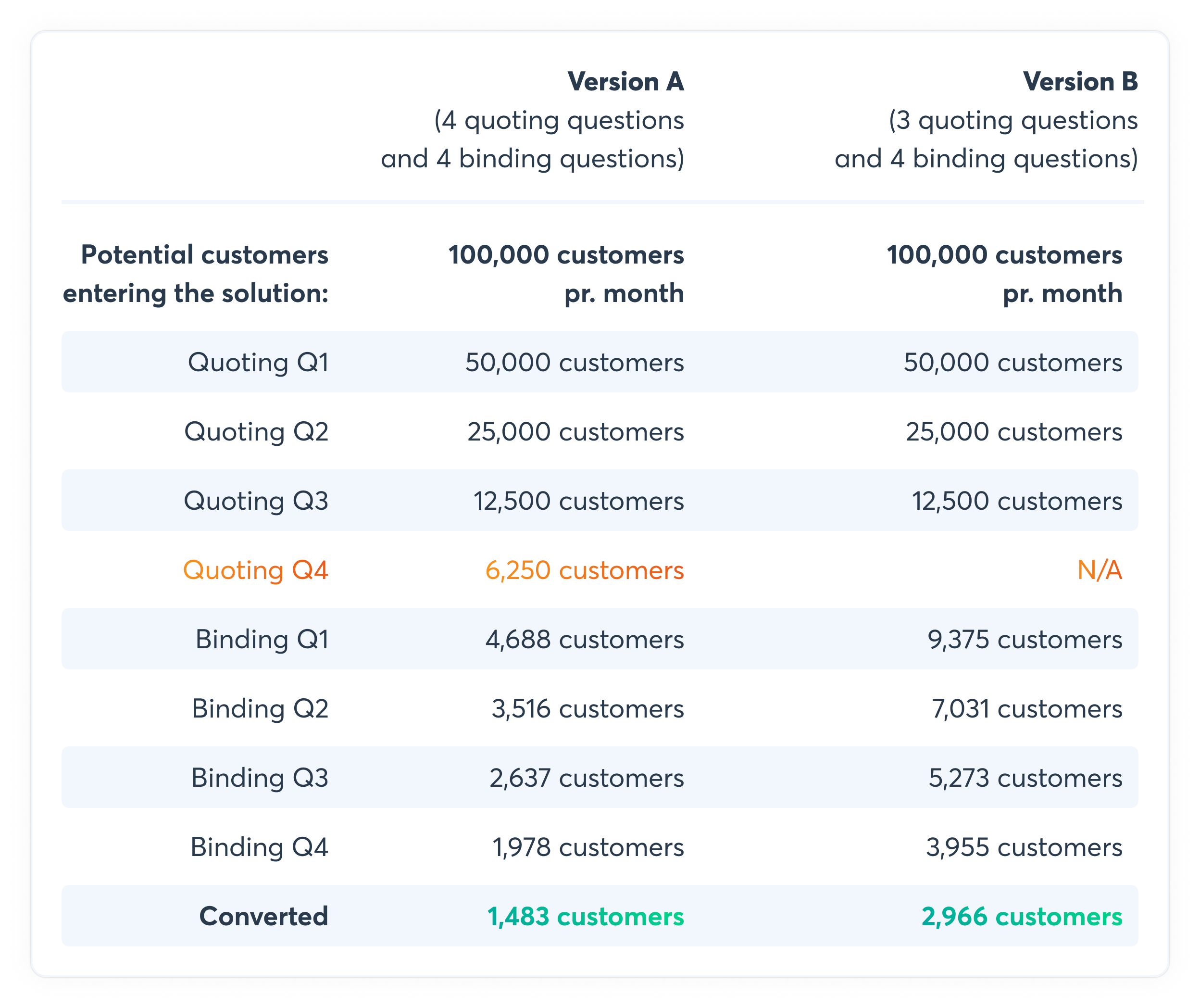

On a rough estimate, you lose half of your potential sales with each question you ask customers before providing them with a quote. And you lose another 25% with each question you ask after showing them a price.

To put it simply:

So by leaving out only one(!) question at the top, you would be able to double your sales per month.

Of course, it is not always the case that the Product, IT, and Legal departments are just going to let you discard a risk parameter, so let’s take a less radical approach: Default and confirmation.

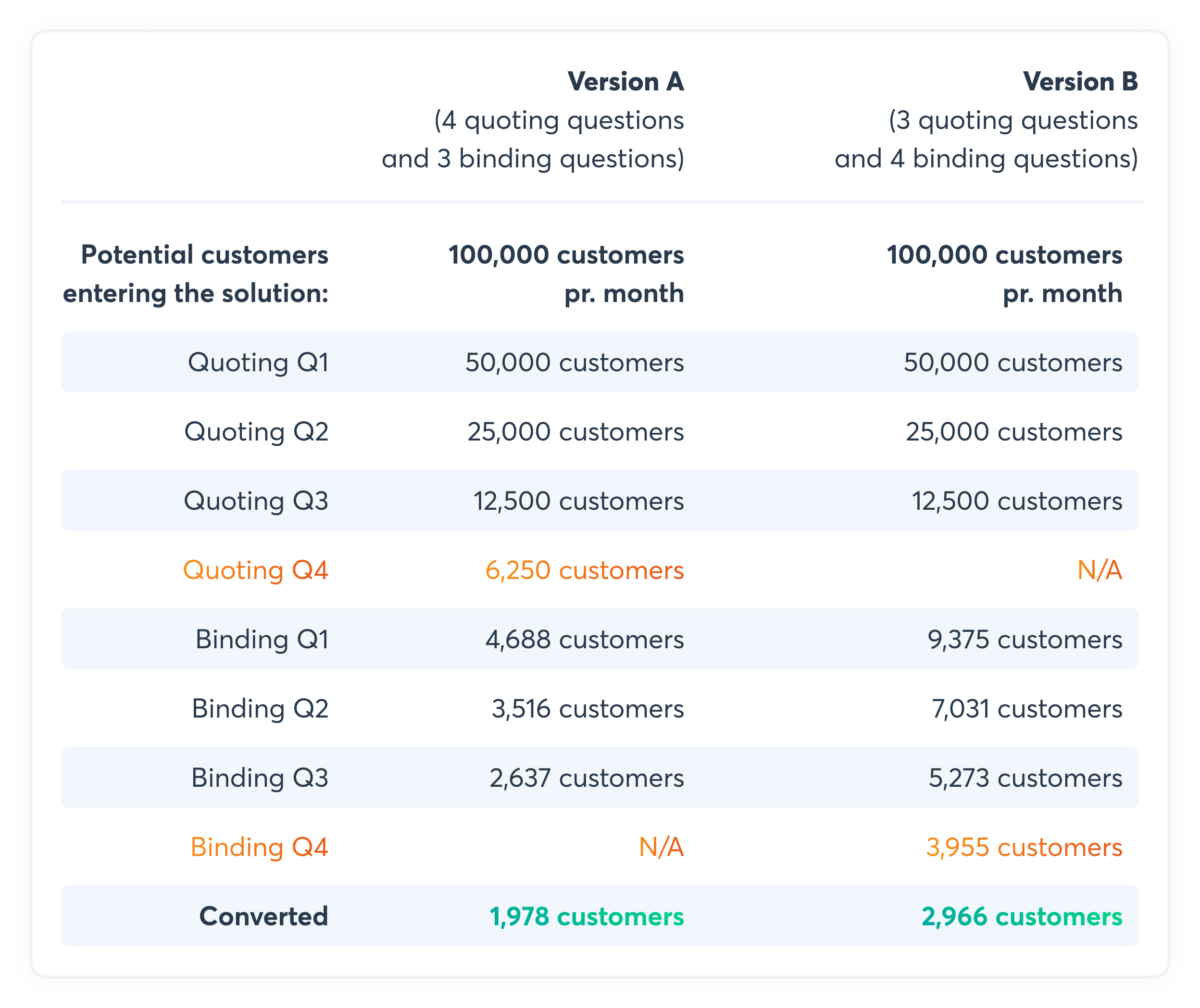

Suppose that Quoting Question #4 has the same answer for 90% of the customers. In that case, why not default to that answer in the quotation process and ask potential customers to modify the default value during the checkout process. At that point, they were a little more committed to the product and less likely to be scared off by the additional inquiry.

Here’s a simple table of defaulting the answer to Question #4:

Here, defaulting the answer to a single question results in 50% more customers per month. The voice of underwriting reason would object that you have presented 10% of customers with the wrong price upfront. Won’t changing the price during the checkout process leave them annoyed and less likely to purchase?

Let’s suppose that’s the case. The worst-case scenario is that those customers will click away without purchasing. Even without that additional 10%, you’ll still acquire 634 customers per month, which is roughly 35% more sales.

Moreover, it might be that the price actually goes down for half of those customers and they gladly purchase your product. Now, you have 669 customers per month. That’s 43% more customers every month, simply by moving Question #4 further down in the underwriting journey.

I’ll admit that this is simplified. After all, you’ve got a lot of similar tools to put in play, such as:

- Showing the default at a step where the customer can see the price, where the customer can modify the default value and change the price accordingly.

- Offering ranges instead of asking open questions.

- Asking more simple questions as boxes to be checked when purchasing.

- Prefilling the forms with your best guess or the most commonly used answer instead of presenting customers with blank fields they have to fill in.

- Giving help tools to assist customers in finding the answer to less obvious questions.

But overall, the optimal approach is to look at each question from the customer’s perspective and use your data to see if there might be a better strategy for handling that specific question.

Hunting for bad apples kills your conversions

So, to sum it up: Many insurers ask extra questions to spot fraudulent behaviour before the customer has even purchased the insurance product.

I’m sorry that I have to be a party killer, but when you hunt for the bad apples, you’re also killing your conversions.

The worst part is that this bad habit is a vestige of the older analogue process, which doesn’t take into account the new medium of distribution.

Don’t get me wrong, I understand the instinct to be wary because people are going to commit more fraud with online insurance than they are with products purchased directly from an agent. Especially, if they can file a claim online as well.

But before you ask potential customers to upload a picture of themselves holding a receipt that is less than 14 days old, the insured product, and a government-issued I.D., ask yourself: Assuming that less than 0.1% of people are willing to commit insurance fraud in the first place, how many of them end up in a position where they can actually do it? Wouldn’t it be financially sound to pay out one or two fraudulent claims a year if it meant you could sell twice as many insurance products?

Plus, you can set up fraud detection systems that catch false claims after the product has been purchased instead of bothering every potential customer with extra questions.

Don’t kill your conversion rates just to hunt down a few bad apples. If you do, you might find yourself with half a bushel instead of a full one.

If you need any help by making your customer journeys customer-centric - without messing with your underwriting - you’re more than welcome to book a free demo with our specialists.

Get a full understanding of what Embedded Insurance is.

Special thanks to our expert Simon Bentholm.