Dealing with acquisition cost is like dealing with a lockdown haircut: You want to cut it, but it's easier said than done. Maybe we can help you (with your acquisition cost, not your haircut). In this article, we give the value chain an upgrade to show you why digital embedded insurance can send your acquisition cost in a free fall, raise your technical result, and, oh well, future-proof your business.

If you say ‘digital embedded insurance’ to global insurers, they feel the tickles in all the right places. (And so do I, btw).

Sure I’m happy that many in the industry engage in the boiling hot subject. But…

I’m also a bit wary when it comes to jumping on the bandwagon with a lightweight buzzword approach.

As opposed to some industry trends, digital embedded insurance is not a fancy-schmancy hype.

Therefore, my colleague in crime, Simon Bentholm, and I have plunged into a series of articles. In these, we take a deep dive into the financial impact of digital embedded insurance.

In the first volume, Simon covered how digital embedded insurance is the only distribution method that can offer an exponential scale of economics.

This is my cue. And raises the million-dollar question:

- What are the bottom-line economic gains of investing in embedded insurance?

The short (and already revealed) answer is: The gains are that you cut down the acquisition cost per insurance sold compared to other distribution channels.

The acquisition cost can be defined differently from company to company. In this article, we stick to a general definition, i.e., the cost related to marketing, selling, and onboarding a new customer.1

The reduction in this article is defined for P&C private lines. There’s a chance that the model is also applicable for commercial lines up to 15 employees (+/-) within known risk groups - i.e., excluding risks that need speciality UW, for instance, Marine Insurance.

The economic gains come from reallocating your digital marketing budgets into partnerships - and not increasing the marketing budget. The impact of investment will put customers on a first-name basis with your brand (which rhymes with brand awareness). It will also boost your number of digital sales.

The way to the brand heaven described above is paved with four elements: 1) The market, 2) distribution channels, 3) market impact on distribution and 4) acquisition cost development.

Looking from where I’m standing, there are strong reasons to believe that these four variables will create good conditions for lower acquisition costs to happen. I’ll involve you in my forecasts in a moment. But to get off to the best start, I’ll shortly coat you in the figures and data that form the basis of my forecasts.

A man and his calculator

In this article, I imitate a common approach to cutting acquisition costs for non-life insurance. Meaning that I present and develop the embedded sales channel within the insurance omnichannel distribution model.

For the sake of simplicity, I’ve assumed that the P&C market size is unchanged. This means that the framework does not account for a rise in sales of new and existing products nor for price increases.

The figures you’re going to indulge yourself in, both in this and the following sections, are based on a mix of Penni.io’s own three years of data and data from ‘the big boys’ in the industry.

The examples used in this article result in a cut of 0.5% in a combined ratio by the end of 2025. This is when the embedded sales channel is to account for 4.1% of the total annual sales.

(For the number nerd inside you: The 0.5% is a result of how I expect the market behaviour for buying insurance to develop x sales costs today x expected savings on sales by reallocating marketing investments and, by that, changing the sales distribution. The 4.1% is the goal of turning offline distribution channels into digital embedded sales channels).

The action needed to realise this gain is to develop the digital marketing activities within the embedded channel. It’s also to put more focus on relevance, driving traffic, and placing. In other words: To do some marketing magic by turning a point of interest into a point of sales (Harry Potter, go home).

By using existing traditional and new digitally engaged partners, we count the embedded sales channel to have up to and not limited to 40% lower costs than existing distribution channels - i.e., agents and brokers.

Sales via the embedded channel will come at the expense of ‘high street brokers and agents’ who lack a digital maturity in the way they approach their marketing and engage their customers.

But just to set the record straight: This is a ‘service check’ of the omnichannel distribution model. It’s not a disruption of the existing channels. Brokers and agents will still be a dominating force in insurance distribution in 2025.

Looking into the crystal ball (spoiler alert: I see embedded sales channels)

In 2020, Simon Torrence - senior advisor on organisational growth and digital innovation - wrote this piece on embedded insurance. He expects the embedded sales channel to account for a $3 trillion market over the next 10 years.

This points out the potential that the embedded channel offers via various types of embedment strategies.

Insurance sold via third parties is nothing new. Affinity and other B2B2C models are a well-founded part of the insurance industry.

However, the digital embedment paves the way for a competitive and future-proof business. It does so because it offers opportunities the market has not experienced - or thought of as possible - before.

Digital embedment strategies can vary.

In this article, I focus on linked and related embedded sales strategies. Using the linked strategy, you sell insurance at an existing point of sales of the B2B2C part. Following the related strategy, you sell insurance at a point of interest. This means that the insurance relates to the product and can be relevant (for the customer) to offer.

The mix of the market and tech developments opens a not-seen-before opportunity within marketing and sales.

Further, it’s not ‘only’ possible to engage customers at point of sales (classical insurance B2B2C sales approaches). It’s also possible at any point of interest (classical AIDA model: Attention, Interest, Decision, Action) by helping the customers in their decision and action processes.

This goes hand in hand with the consumers who, in recent years, engage more and more digitally in their (re)search and purchase process for services and products across industries. It therefore also opens up new - and more beneficial - opportunities for the marketing and sales efforts for insurance.

If the insurance industry is to grasp these opportunities, the market needs to enable and encourage online sales behaviour ongoing. As we mentioned earlier, certain things have to be in place to make the embedded insurance sales channel thrive. And be the star of the show.

But from my point of view, it’s not a matter of ‘if’ but ‘when’. There are signs, trends, and changes in the insurance landscape pointing in the same direction.

So, now that you’ve soaked up a lot of valuable data and insights, you’re ready to take the next step (into the future) with me. Let’s start with the market.

Free download: Why digitising insurance partnerships is essential for sales growth

Forecast #1: The market

Across industries and countries, we’ve seen a rise of over 125% in the past 5 years in customers' digital engagement and purchases of goods and services online.

In the coming years, we can expect to see e-commerce grow by 21.8% of total global retail sales.

This tells us of how consumers worship - and trust - the e-commerce shopping experience.

It can also be used to foresee how this will reflect on online sales of insurance by showing the number of consumers in the market who are ready to buy online. This is where we see the Mount Everest-high potential of embedded digital sales.

-1.png?width=500&name=Development%20of%20e-commerce%20share%20of%20total%20global%20retail%20sales%20(1)-1.png)

Source: Statista.

Let’s assume two things:

- That the overall growth will be as shown until 2024 and be stable for 2025.

- That the insurance industry you work in continues to see the gain of using the online sales of insurance as a distribution channel.

Then the next step is to predict how much the online sales of insurance will grow compared to the overall growth of e-commerce sales. Question mark.

This is a tough one. And I’m crunching numbers as I write and you read.

However, I doubt that the growth will be 1:1 with the overall e-commerce growth. This is predicted to be 13% for the coming years. Yet, I expect it to rise compared to the past 5 years. But by how much and how quickly, I’m still hesitant.

Therefore, for this calculation, I predict that the rise in digital insurance sales will be 6% year over year.

This prediction matches 50% of the overall e-commerce growth but also shows that insurance is a slower mover than other industries. However, it’s on the rise.

Forecast #2: Distribution channels

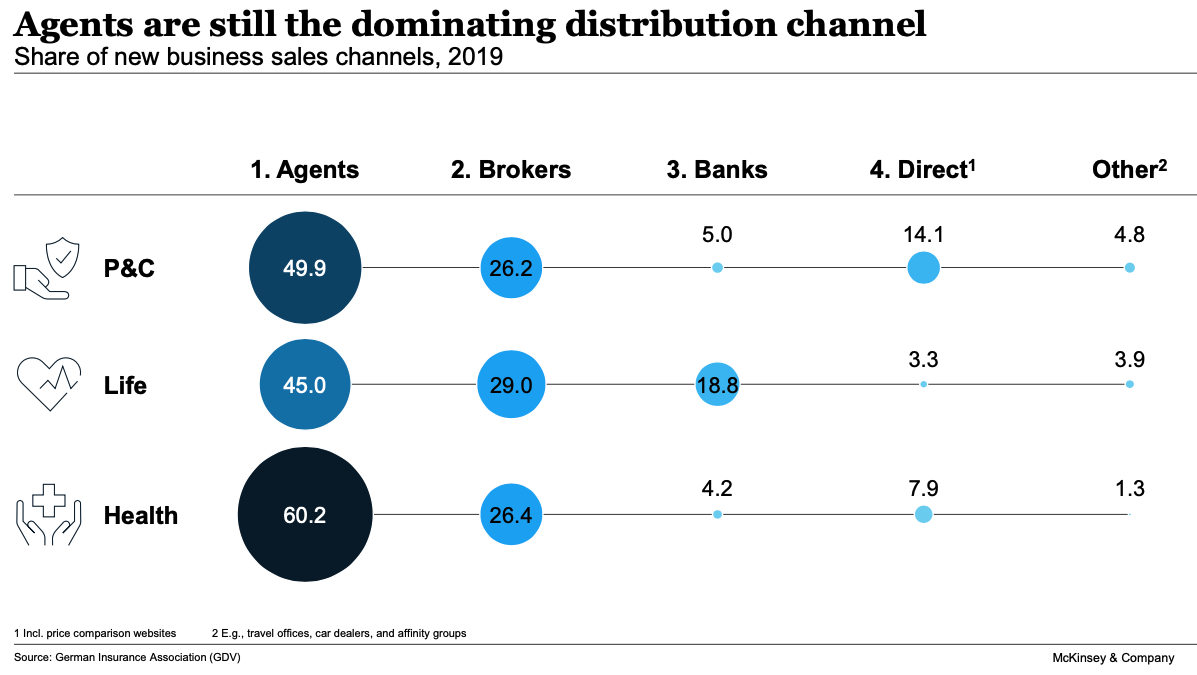

Below is a table showing the distribution mix. This is described by Mckinsey in their insurance industry report for Germany, April 2021, based on numbers from 2019.

I see these numbers fit most insurance markets since brokers and agents still dominate. I expect these to continue to dominate as the preferred insurance distribution channel for P&C until the end of 2025.

Therefore, to the market forecast, 6% of sales that happen today through brokers and agents will in the coming years move to online channels - i.e., direct and embedded channels.

Forecast #3: Marketing impact on distribution

No matter which channel, the key driver for marketing efforts in the coming years is to:

- engage digitally with customers.

- gain from the shift in the purchase behaviour simulated above.

The ability to engage customers in the digital space will vary from channel to channel. But in any case, Simon and I predict that the agent and broker market will be split in two:

Agents and brokers who don’t invest in digitisation will see less offline customer ‘traffic.’ Agents and brokers who already engage in the digital space will not see fewer client meetings. I also believe that the result of this is fewer agent/broker distribution channels as consumers are aware of other ways to buy insurance. But let’s save this for another article.

The lack of digital skills with some brokers and agents will be larger than the rise in skills of other brokers and agents.

Added to this, the fact that consumers engage more and more digitally will have a good effect on digital-born offers. These include direct sales or more interesting (and cheaper) embedded sales channels which could be offered by the digital-first brokers and agents. Thus, the digital slow movers will lose the battle.

Ouch.

And I might be hitting another soft spot by saying this: The agents and brokers that risk losing digitally engaged leads are ‘high street brokers and agents’. They’ll lack digital skills to support customers in their native digital environment. To put it in a nutshell, they, therefore, rely on locals walking into their shop from the street.

Forecast #4: Acquisition cost development

If we assume that the shift in the purchasing trends will favour online direct channels and embedded digital channels. Then the insurance sellers should now look at how to use their marketing efforts to improve sales conversions in these channels.

As illustrated in volume 1, the cost of driving traffic to own online sales channels has supported Google earnings for many years. Therefore, this marketing channel holds potential and needs development in order to cut down the acquisition cost. And digital embedment is the middle way to take the channel to the next level. Marketing insurance to end customers in your partner's digital universe, and hereby not competing with competitors for attention.

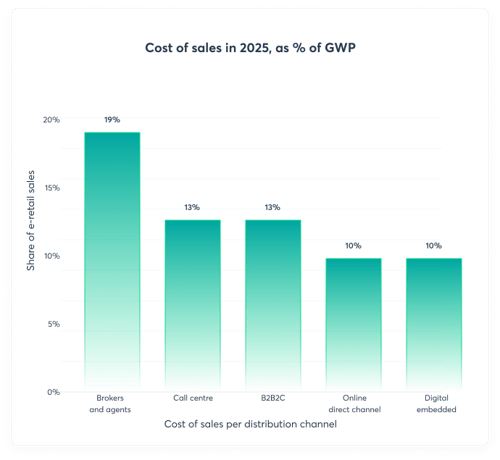

In the graph below, I use an acquisition cost benchmark on the basis of a tier 1 insurer general report from 2020. The cost is shared as a percentage of total GWP (not isolated first-year premium) at 17% of GWP.

It’s not clear from the report what is the proportional acquisition cost per P&C segment and if marketing is included. For this simulation, the acquisition cost includes marketing costs. I’ve simulated other channels acquisition costs, based on the Mckinsey distribution channel mix, to reach 17%.

Based on the Mckinsey distribution channel mix and Tier 1 Annual report from 2020.

The assumptions behind the channels above are:

(A) that call centres talk to more customers per day. This trim costs compared to agents and brokers meeting face to face.

(B) that distribution partners (embedders) are motivated to sell insurance in order to either (or both) upgrade their long term customer lifetime value and grow short term revenue. It’s my experience that the B2B2C channels cost less in marketing and commissions. For this example, I, therefore, lean towards call centre cost levels.

(C) that online direct sales cost is low as a result of nearly zero sales commission cost. However, marketing costs are sky-high. For this example, I expect (D) that digital embedded will be on par with online direct year 1. This is due to the investments needed to develop both the technology and partner network to deliver and run a successful embedded channel. As mentioned in volume 1, this number will drop over time as scale effects and marketing gains kick in. These gains are not seen in other marketing channels.

The result of a settled embedded insurance channel

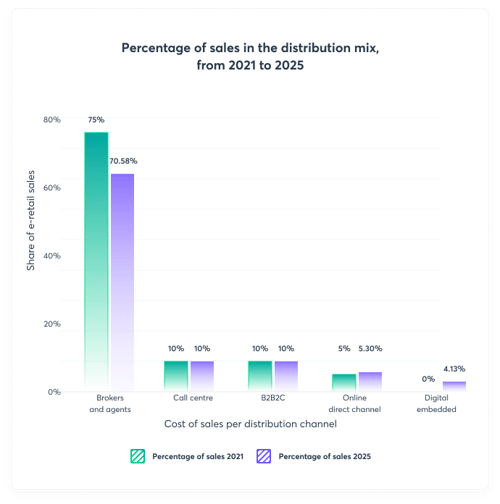

These four forecasts will result in a gradual development of the distribution mix. By 2025, the digital embedded channel will considerably rise and direct online sales will experience minor growth. Both to the expense of brokers and agents.

By embedding insurance offers into consumers' existing digital mindset and behaviour, you get the chance to cut down your acquisition costs.

Based on the Mckinsey distribution channel mix and Tier 1 Annual report from 2020.

I estimate the benefit by the end of 2025 is given the above to be 0.48% of GWP on the portfolio if 4.1% of total sales in 2025 comes from digitally embedded sales channels. So, if your GWP is, for instance, €5 bn, the technical result will rise by €25 m. That's not so bad.

.png?width=500&name=Decrease%20in%20cost%20of%20sales%20associated%20to%20an%20increase%20in%20digitally%20embedded%20sales%20(1).png)

Based on the Mckinsey distribution channel mix and Tier 1 Annual report from 2020.

The detail-oriented reader would argue:

- that a market rise in digital involvement by customers must affect online direct sales more positively than we have simulated

- that every channel has a different customer lifetime value, which will affect the result.

I agree. And agree to disagree.

- There could be a spin-off to the direct channel from a boost in general digital customer engagement. However, the embedded channel will profit 100% from the investments made into these channels.

- CLTV does not affect year 1 acquisition cost. It’s a topic to be handled under churn and the developments that are underway in your churn initiatives.

I hope you felt the tickles. And are up for another round.

Because the next financial article - volume 3 - is action-packed. Not in the ‘James Bond trying to escape the gunfire of a handful of villains’ kind of way. No, we’re literally going to cover the actions that you need to take to cut down your acquisition costs. In other words: You can look forward to a how-to article that’ll add to what you’ve read in this volume.

Special thanks to our expert Esben Seyffart Sørensen.